Story Highlights

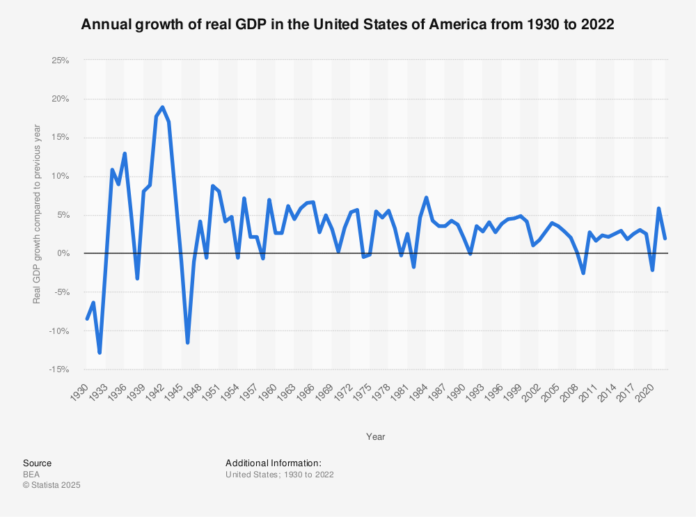

A delayed government GDP report showed the U.S. economy grew at a 4.3% annual rate in Q3.

Strong consumer activity led the expansion, reinforcing the economy’s resilience despite mixed signals elsewhere.

Markets and policymakers are weighing what strong growth means for inflation risks and rate decisions.

A long-delayed GDP release showed the U.S. economy expanded at a 4.3% annual pace in the third quarter—its fastest growth rate in roughly two years, according to The Wall Street Journal’s market coverage and analysis. The standout factor is consumer strength: households continued spending at levels that lifted overall output, even as investors and analysts monitor whether the momentum can hold into year-end conditions.

The key point is that consumer-driven expansions tend to be both powerful and fragile. Powerful because consumer spending is a large share of U.S. GDP; fragile because it’s sensitive to jobs, wages, credit conditions, and inflation expectations. The report’s headline number is a strong snapshot, but markets typically treat GDP as one part of a broader mosaic—especially in a period where inflation concerns and labor-market cooling can pull policy in opposite directions.

Why it matters is the policy tug-of-war it creates. Strong growth suggests the economy can tolerate tighter financial conditions, which can argue for caution on rate cuts. But if inflation remains sticky—or if future data show spending is being propped up by temporary factors—then the “best” reading of the report changes quickly. The WSJ framing around the report highlights how investors interpret such releases: not merely as a scorecard, but as a clue about where rates, borrowing costs, and corporate earnings expectations might settle.

The geopolitical implications are indirect but real. A faster-growing U.S. economy can support stronger defense outlays, higher import demand, and greater leverage in international economic negotiations. But it can also increase global interest-rate spillovers—higher U.S. yields can tighten financial conditions abroad, particularly in emerging markets. Meanwhile, resilient U.S. demand affects global commodity flows and trade balances, shaping how partners and competitors plan their own fiscal and monetary paths.

The more immediate watch item is what comes next: whether Q4 slows as delayed data normalize and whether consumer strength persists amid shifting confidence and job-market signals. GDP can tell you the economy was strong; it doesn’t guarantee the economy will remain strong. That’s why subsequent readings—retail sales, jobs, inflation, confidence—often determine whether a “hot” quarter is the beginning of a trend or the high-water mark before deceleration.

Implications

If consumer spending remains durable, the economy may carry more momentum into early 2026 than many forecasters expected—raising the bar for rapid rate cuts. If spending cools, markets may treat Q3 as a late-cycle surge rather than a stable runway. Either way, the 4.3% print strengthens the argument that U.S. growth has been more resilient than many “slowdown” narratives suggested.

{kind=link}